Simon Molloy

February 2026

BIG TECH, LITTLE COMPETITION

Since the 1950s, beginning with the IBM dominated mainframe computer era, the world has watched successive waves of tech booms but to AI boom is different in a fundamental way: it’s much more competitive.

The personal computer era was supposed to democratize information processing. Instead, Microsoft captured the market so completely it faced antitrust action by the late 1990s. In those days Apple was just a bit player.

The Internet was going to be an open commons of human knowledge. Today, Google has captured over 90% of global search, while Meta’s platforms mediate the social lives of three billion people. Search and social media, it seems, were highly susceptible to monopolisation.

Although other players tried to enter the smartphone market (remember Amazon Fire?), it quickly collapsed into the Apple Android duopoly.

These outcomes weren’t accidents. They were the predictable result of fundamental structural characteristics of these markets: economies of scale, network effects, high switching costs and winner-take-all dynamics.

The AI revolution, however, appears to be following a different script. For the first time in computing history, we’re witnessing a genuinely competitive technological boom – one where multiple players with distinct approaches, philosophies, and business models are vying for dominance without any single entity approaching monopoly status. Moreover, significant drivers of future monopoly outcomes have yet to emerge.

This competition also extends across national borders and, indeed, is seen widely as a driver of geo-strategic outcomes.

This critical difference, if it persists, could fundamentally alter the relationship between technological innovation, consumer welfare and the returns to those trillions of dollars of AI investment.

MARKET POWER IN TECH HISTORY

Economists are very interested in competition, because it’s competition that delivers the benefits of markets to consumers. In any Economics 101 course you will find the classic description of the spectrum of decreasing competitiveness (and increasing market power) from the theoretical optimum of perfect competition through monopolistic competition, oligopoly, to pure monopoly.

Perfectly competitive markets are rare if they exist at all (other than in the minds of economists). Usually, market structures end up somewhere between the polar cases of monopoly and perfect competition.

What makes the current AI moment distinctive is that it appears to be settling into a market structure of genuine monopolistic competition: where many firms offer differentiated products (Claude vs ChatGPT vs Gemini vs xAI vs DeepSeek) with, and this is critical, relatively low barriers to consumer switching. Each firm commands some market power through product differentiation rather than via scale and network effects.

In contrast, Microsoft’s triumph in personal computing grew out of its cultivated application ecosystem: as more users adopted Windows, more developers wrote Windows software. As more Windows software became available … you know how it goes. The natural monopoly characterises of operating systems was also crucial (why on earth would we want ten OSs?).

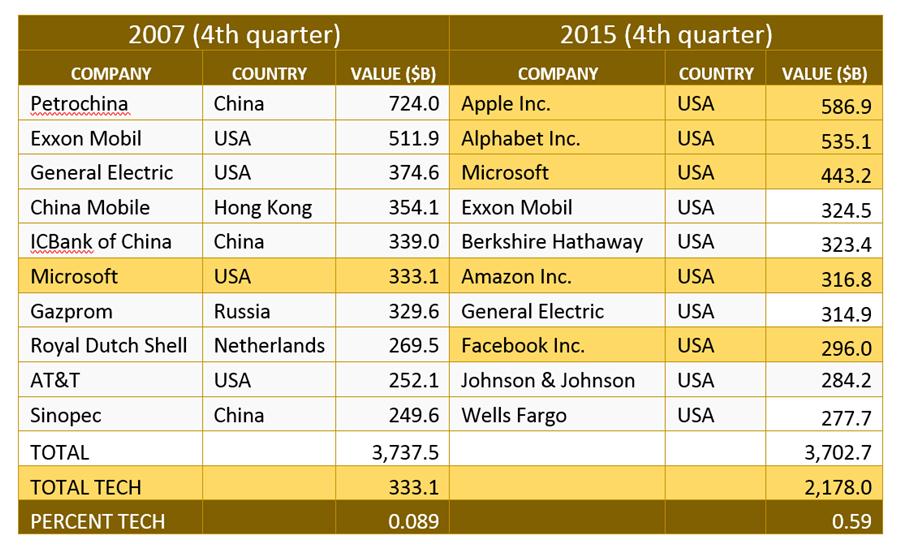

It took Google half a decade to achieve such dominance that it became a new verb. Facebook managed to destroy virtually every social networking competitor, from MySpace to Google+ and absorbed Instagram and WhatsApp while regulators were scratching their heads trying to understand digital dominance.

The pattern is clear: a technological wave may begin with apparent openness and competition but then, because of underpinning structural features, these markets rapidly consolidate around one or two dominant players who capture the majority of economic value.

The market power of the winners is manifested in their incredibly high margins. Microsoft reached peaks near 45% in the 2000s, while Google’s search business earned gross margins of 75%. These levels dwarf traditional industries where automakers operate at 5-10% margins and retailers often below 5%.

So, the trillion-dollar question is: will AI’s monopolistic competition collapse into duopoly or be dominated by a single player? The answer to this question is central to determining how the benefits of AI will be distributed between AI investors and consumers of AI services.

THE STRUCTURAL DIFFERENCES OF AI COMPETITION

Several factors distinguish the current AI boom from its predecessors, and these differences appear structural rather than merely circumstantial. Creating a competitive search engine in 2010 was nearly impossible; Google’s head start in indexing the web and understanding user intent was insurmountable. Building a competitive AI model in 2025, by contrast, requires significant capital, computational resources and talent, but these inputs are available to multiple players. The models themselves, once trained, don’t benefit from the same kind of network effects that made Google’s search algorithm better with each query and Facebook more attractive with each additional user.

More fundamentally, AI lacks the natural monopoly or network characteristics of previous platforms. ChatGPT doesn’t become more valuable to me because more people use it. Claude doesn’t improve for individual users because Anthropic gains market share.

The main driver of this characteristic would appear to be the separation of training and inference in AI models. Any innovation in AI models that improves performance based on interactions with users would create network effects that could lead to market dominance. But that’s not how LLMs work. Not yet, anyway.

It’s tautological to say that, in the world of hyperscaling, economies of scale matter. While economies of scale can drive consolidation, in the case of AI, there is no clear early entrant that looks set to win the race for scale. Moreover, economies of scale don’t necessarily lead to winner-take-all outcomes, especially in very big markets. The automobile industry, for example, exhibits huge economies of scale but there are still many auto producers around the world.

The current AI market manifests this openness. Google, despite being an incumbent tech giant, isn’t running away with the AI market. Industry colossus, Microsoft, through its partnership with OpenAI, has tried to reenergize its consumer offerings but hasn’t achieved dominance. OpenAI, the apparent early leader, faces serious competition not just from tech giants but from well-funded startups like Anthropic and xAI. And then there’s DeepSeek.

Even the business models remain unsettled. Some companies offer subscription services directly to consumers. Others focus on API access for developers. Some pursue advertising-supported models, while others avoid advertising entirely and emphasise security and privacy.

WHY THIS MATTERS FOR CONSUMERS

The persistence of competition matters enormously for end users, and not merely because it keeps prices in check. Monopolistic tech platforms have consistently demonstrated that once they achieve dominance, the innovation that serves user interests takes a back seat. Facebook’s steady degradation of the user experience in favour of algorithmic content and advertising offers a clear example, as does Microsoft’s lazy last two decades of the twentieth century.

Competitive markets, by contrast, must continue innovating to retain users. When Anthropic emphasizes safety and controllability in Claude’s design, it’s not merely virtue signalling, it’s competitive differentiation. When Google integrates AI into search, it’s defending against the possibility that users might abandon search for AI-native information discovery. The bottom line? Consumers win.

CAUTIONARY TALE FOR INVESTORS

The message for investors, however, is less rosy.

It may be that tech investors may have an unconscious assumption that all tech companies will have the market power that they have enjoyed in the past – the deep wide moats around market shares and the associated persistently high margins.

But what if AI company profit rates look less like Google advertising and more like main street retailing?

There’s no shortage of financial pundits claiming that AI is an investment bubble; that AI revenue can never repay the stupendous investments.

What kind of assumptions about margins are these pundits baking into their prognostications? Harris Kupperman, Founder & Chief Investment Officer of Praetorian Capital Management, who argues the boom is a bubble, speculates: “say that ultimately, the margins get to positive, and then gradually creep up towards 25%. Why 25%? I have no idea. It just sounds right.”

There aren’t too many retailers on the planet who wouldn’t kill for a margin of 25%.

If a critic of the boom assumes 25%, what are the boosters assuming?

Competition means lower prices and lower prices usually mean lower margins and revenues. If AI’s market structure ends up being more like monopolistic competition and less like monopoly, the prospects of investors ever making a return become much much dimmer.

For emphasis, it doesn’t matter how good AI gets, how much value it adds; in a competitive market revenues are pushed down towards costs and margins stay low.

UNCERTAIN AI ROAD AHEAD

There is no guarantee that AI will remain as competitive as it is now. Network effects could emerge in unexpected ways. The enormous computational resources (including electricity) required for training frontier models might ultimately be accessible only to the largest tech companies, creating an effective oligopoly by resource constraint rather than market dynamics.

The structure of the current moment is genuinely different from tech booms we’ve seen before. The absence of strong network effects, the low switching costs, the genuine diversity of well-funded competitors, and the ongoing uncertainty about which business models and technical approaches will prove superior are factors creating conditions for sustained competition that previous technology revolutions lacked.

Or maybe a bursting bubble will, in the end, force consolidation, in which case some investors will win and others will lose.

But maybe AI will turn out to be, like so many other industries, competitive enough to shift value and benefits in the direction of consumers rather than shareholders.

Could AI be the first pro-consumer tech boom?

Maybe this is, finally, the revenge of the nerds.

Simon Molloy is Managing Director of Systems Knowledge Concept, an Australian technology and communications economics consultancy.